Good morning!

First off, a big thank you for all the feedback you sent through. There were some very kind words in there, and I showed my mum. She was stoked.

Today, I thought we would take a step back from the news and answer some of your questions. There were lots about the share market and inflation, so this week we have a mini crash course on these topics.

Without further ado, let’s go!

Your questions, answered

Question: Help! I need a beginner's guide to the share market

Dear questioner, you are not alone in needing this. Let’s walk through it step-by-step.

First, what are shares?

Imagine you want to start a business selling coffee with your friend, Zara. Under Australian law, you have a few options: be a sole trader (just you), set up a partnership (like a law firm), or start a company.

Let’s say you go with a company. In Australia, all companies must register with ASIC - the Australian Securities and Investments Commission. When registering, you have to list who owns the company. These owners are called shareholders and they each own a slice of the company, called shares.

So, you register your coffee company and list yourself and Zara as shareholders, give yourself 1 share each, and now you each own 50% of the company.

Where do people buy shares?

Let’s say the company is growing quickly, and you want to open more stores, but you don’t have the cash. What do you do? You have two options:

Borrow money. You go to a bank and borrow money, which you have to pay back, with interest.

Sell a slice of the company. This means issuing new shares to an investor in exchange for money. You don’t need to pay it back, but they now own a part of your company and are entitled to a share in the profits.

Let’s say you go with option 2 - selling shares. Where do you find the buyers?

At first, you might do it privately. You pitch your business to friends, investors, or venture capitalists. This is called raising private capital (in this context, capital = money), and the shares are bought and sold behind closed doors.

But as your company grows, you might want to access more investors. That’s when you “go public” and list your company on a public sharemarket, like the ASX - Australian Stock Exchange. This is called raising public capital. Now, anyone and everyone can buy your shares.

The big four banks all offer platforms where you can buy and sell shares. These platforms let you trade shares on the ASX, and they can link to your bank account for easy transfers. There are also non-bank affiliated platforms, such as SelfWealth, Superhero, and others. These are often called online brokerage accounts.

Why do people buy shares?

Because they want to grow their money. If you buy a share in a company and that company does well, then your little slice becomes more valuable. You can sell it later for a higher price (that’s a capital gain), or sometimes the company gives you a share of its profits directly (that’s a dividend). Either way, the idea is, invest now and hopefully earn more later.

How do they know what to buy?

Well, they don’t really know, not for sure. But people take different approaches to try and make money:

Active investing means picking individual companies you think will do well. There are different strategies here — some people buy shares in companies they believe are undervalued and hold them long term. Others look for small companies they think are about to take off, or ones that pay big dividends so they can earn steady income.

Passive investing means you don’t try to pick winners. Instead, you follow a rule — like buying a tiny slice of the biggest 100 companies on the stock exchange. Some companies will rise, some will fall, but the idea is that over time the winners outweigh the losers, and you come out ahead.

One important thing to keep in mind: what people buy often depends on how much risk they’re comfortable with. Active investing can be riskier because you're betting on a small number of companies — and if one of them crashes, so does your investment. But with passive investing, you usually spread your money across lots of companies at once, so if a few do badly, the others can help balance it out.

That spreading out of risk is called diversification, and it’s one strategy investors can use to protect themselves. But there are also some risks, like random shocks that affect the whole economy e.g. pandemics, and that cannot be diversified away.

It’s a beast of a topic, so let me know what else you are keen to learn about the share market!

A message from EatClub

Not ready to invest in the share market? Start by investing in dinner.

We get it - stocks, ETFs, dividends…it’s a lot to learn. But while you’re wrapping your head around how the share market works, here’s one return you can count on: up to 50% off your next meal with EatClub.

It’s a free app that helps you save big at restaurants and bars across Australia. Just pick a deal, eat and drink well, and pay with your EatClub card - the discount applies instantly. No risk, all reward.

With over 3,500 venues to choose from, you’ll be eating out for less while everyone else is still trying to work out what a bear market is.

Download EatClub. Your portfolio (and your stomach) will thank you.

The week’s biggest finance headline, explained

WTF is inflation, and why does it matter?

Great question. I’ll get to the answer, but let me start with some background. Last week, the Australian Bureau of Statistics (ABS) announced that inflation was 2.4% in April. What does that actually mean?

First, what is inflation?

Inflation is a concept in economics that refers to the rate at which prices are rising across the economy.

Imagine an economy where the only thing for sale was a Taylor Swift t-shirt. Let’s call this economy “Taylor Mania”. In January 2025, the t-shirt cost $100. But in January 2026, it cost $110. The price of the t-shirt increased by $10 over a year. So we would say the rate of inflation in Taylor Mania is $10 per year. Or, to express it as a percentage increase from the original price, $10 divided by $100 = 10%. So inflation in Taylor Mania in January 2026 is 10%.

This is the basic idea behind how the ABS calculates inflation in Australia, but it’s slightly more complicated when you add multiple items.

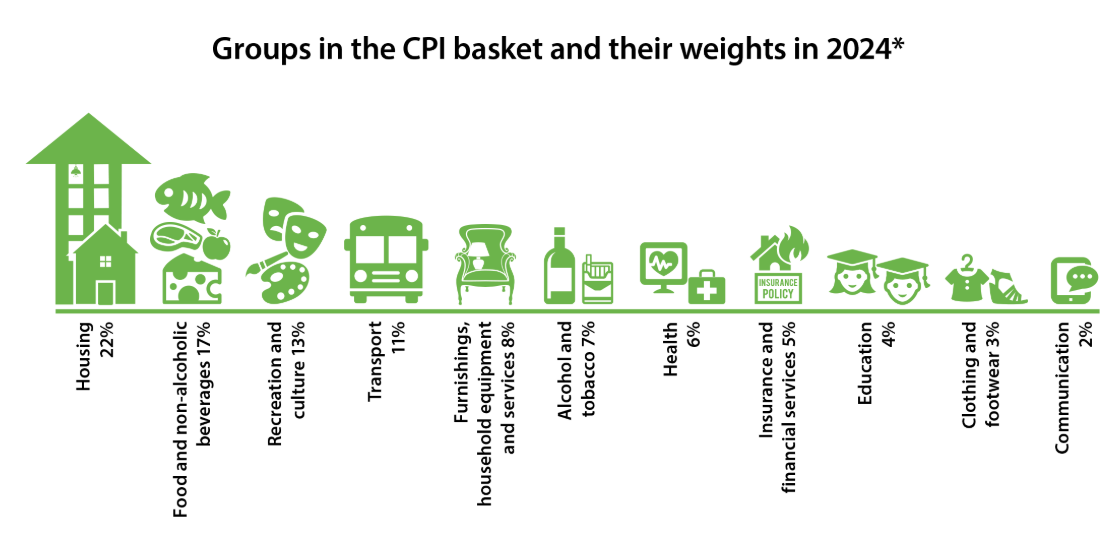

First, they make a big list of things that people usually spend money on—like rent, groceries, insurance, and cars. This list is called the Consumer Price Index (CPI) basket.

Second, they check how much of a typical household’s budget is spent on each item. Some items, like rent, make up a bigger part of your budget than others, like your phone bill. And so the ABS assigns each item a weight based on its relative importance.

Third, they calculate the price change for each item in the CPI basket.

Fourth, they calculate the overall inflation rate by aggregating all these individual price changes together, based on their weights.

Here is a useful infographic from the RBA on what items are included in the CPI basket and what their weights are:

Note: Numbers don’t add up to 100% because of rounding | Source: RBA

Is inflation good or bad?

The Reserve Bank of Australia strives for low and stable inflation.

Here’s why. If inflation is too low, or prices start falling, people might wait to buy goods and services, hoping they’ll be cheaper later. But if everyone waits, shops don’t make money and might have to fire workers. Then those workers can’t afford to buy things either, and the whole economy slows down, leaving everyone worse off.

If inflation is too high, prices go up faster than your pay. You can’t buy as much, so you ask for a raise. Your boss gives it to you, but then has to raise prices to afford your higher pay. Other workers do the same, and prices keep rising across the whole economy faster than everyone’s pay, leaving everyone worse off.

However, when inflation is low and stable, price changes are predictable, and households and businesses can plan their finances. As a result, we avoid price spirals - both up and down. That’s why the RBA targets 2-3% inflation.

What causes inflation?

The causes of inflation can be put into 3 categories.

Demand-side: When demand for goods (like Taylor t-shirts) jumps higher than supply (of said Taylor t-shirts), then this excess demand increases prices and leads to a higher inflation rate.

Supply-side: When the supply of goods drops below the level of demand, then this shortfall in supply has the same effect.

Inflation expectations: If everyone expects inflation to go up or down, these expectations can be self-fulfilling.

So, how do we control inflation?

The main tool for controlling inflation is the cash rate.

Last week, we talked about why the RBA changes the cash rate:

“When inflation is too high, as it has been, one of the tools the RBA has is to raise the cash rate. This incentivises saving and makes it expensive to borrow money. And with less people spending and borrowing, there is less upward pressure on prices, and inflation eases”

By incentivising saving and making borrowing expensive, the RBA lowers the level of demand for goods and services. This directly addresses the excess demand that may have been pulling inflation higher in the first place.

Why can’t we just print more money?

This might seem like an easy fix - if things are getting more expensive because of excess demand, why don’t we just give everyone more money. Why muck around with incentivising saving or making borrowing more expensive?

Here’s why that doesn’t work — and let’s look at a real-life example. In the 2000s, the government of Zimbabwe started printing huge amounts of money to try to fix problems like poverty and debt. And at first, it felt like a relief. Wages were paid and people had more cash in their wallets.

But here’s the problem: the amount of stuff in the shops - like bread, petrol and clothes - didn’t increase. There was more money, but not more things to buy.

So what happened? People had more money and wanted to buy more. But because there wasn’t more stuff, shops just raised their prices. And people still paid, because they had more cash. And then when they ran out of cash, they just printed more. And the cycle repeated, until eventually a loaf of bread ended up costing millions.

The key idea? Printing money doesn’t create more stuff, it just means there’s more money chasing the same amount of stuff. This pushes prices higher and makes money lose its value.

A titbit for your group chat

Last week, Hailey Bieber sold her skincare company, Rhode, in a deal valued up to $US1 billion. The buyer was another beauty company, e.l.f. Beauty. In the deal, Bieber and her co-founders, Michael and Lauren Ratner, will receive $US600 million in cash, $US200 million worth of stock in e.l.f Beauty, and the right to receive another $US200 million in payouts if the Rhode team hits certain sales targets.

It’s prompted some interesting discussions online about the role of influencers in building the companies of tomorrow. If you’re looking for an interesting read on this topic, I’d recommend this Wall Street Journal profile on Alix Earle, an influencer-turned-business investor.