Good morning!

Can’t believe it’s week 3 of this newsletter already. Week 3 is always a big milestone.

Me during week 3 of TDA: I’m craving feedback on this newsletter. Please leave me your thoughts here.

Me during week 3 of uni: How is it week 3 and I’m already 4 weeks behind?

Me during week 3 of dating my gf: She’s so cool. I hope she likes Gracie (Gracie Abrams for the new readers - we reference her a lot).

Let’s rip in.

Your questions, answered

Question: What does it mean for countries to be trillions of dollars in debt and does it matter?

This question comes from Billi. And it’s a good one.

In lots of countries, debt is at historically high levels. Our government is about $AU1.6 trillion in debt, and last year we paid $AU53.6 billion in interest.

These are some big numbers. Let’s break down what it means.

Debt is money that A borrows from B, with the agreement that it will be paid back in the future, usually with interest (the price paid for borrowing money). So, when we say the government is $AU1.6 trillion in debt, we mean that they have borrowed $AU1.6 trillion and haven’t paid it back yet.

Governments borrow by issuing bonds. Bonds are basically IOUs. Investors lend money to the government by buying the government’s bonds, and in return, the government promises to pay them back later with interest. These investors are usually banks, superannuation funds, insurance companies, other finance companies, and even foreign governments.

Governments borrow money when their expenses are higher than their revenues. That means they are spending more money than they are bringing in.

Imagine you’re in charge of the budget for the Australian government in 2025. You need to pay for things like Medicare, defence, and also cost-of-living relief plans, like energy bill relief. Your budget depends on how much money you can raise through taxes. But what do you do if you need to spend more than you bring in? Well, if you don’t want to cut your expenses or raise taxes, you need to borrow money.

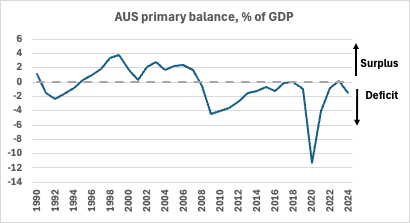

When the government spends more than it brings in, we say the government is running a deficit. And the opposite is a surplus. Let’s have a look at the government’s track record of surpluses and deficits.

Note: Graph shows the Australian government primary balance. | Source: OECD Economic Outlook 117 database.

So, we were in a surplus for most of the 1990s and 2000s, then jumped into a deficit around 2008, and have kind of stayed there ever since (with a big deficit around 2020).

A few reasons. After the global financial crisis (GFC) and during the COVID-19 pandemic, the government spent a lot of money to keep the economy going and support jobs. That’s those two big dips around 2008 and 2019. More recently, cost-of-living support measures (e.g., energy bill relief) is contributing to that small dip in 2024.

These deficits are what cause debt to increase.

No, and yes.

No, because high debt is not necessarily a problem in and of itself. It’s perfectly natural for countries to be in debt. It means they can respond to emergencies, invest in infrastructure, and support the economy during tough times.

What really matters is whether the debt path is sustainable. That means: can the government keep paying off its debt and interest without needing to cut important spending (e.g., Medicare) or raise taxes too much?

Think of it like this: if interest rates are low and the economy is growing, the government can easily afford its debt - like someone with a good job and a cheap mortgage. But if interest rates go up and the economy slows, the debt becomes harder to manage. If that happens, you might need to borrow money just to cover your interest, and then debt is growing faster than the economy.

So yes, because we should always keep an eye on the sustainability of Australia’s debt. And right now, there are a few reasons why we should be extra vigilant. Recently, interest rates have been high, and the economy has been growing relatively slowly (bear with me - we will cover economic growth in a future week).

At the same time, there are lots of future spending pressures from an ageing population, the green transition, defence, and other areas. If we’re not careful, future governments could face tough choices about what to fund, or how much to borrow and tax. But that’s for another week!

Note: All data on debt and interest comes from OECD Economic Outlook 117 database.

The week’s biggest finance headline, explained

Superannuation has been in the news a bit recently. You may have seen that the superannuation guarantee is due to increase soon, and the government is planning to tax super balances above $AU3 million.

Let’s do a quick crash course on super - what it is, its history, and how it works - and then briefly discuss the new changes.

What is superannuation?

Superannuation, or “super”, is a way of saving for retirement that is compulsory in Australia. It means that employers are required by law to pay a percentage of your wages into an account (your super fund), which is then invested over time to help you build up savings for when you stop working.

How was superannuation established in Australia?

Before the introduction of the modern-day super system, Australia’s retirement income system had two main parts:

Age Pension: A means-tested payment from the government. That meant how much you got depended on things like your income, savings, and assets.

Voluntary retirement saving: People could save for retirement on their own. Some employers also set up occupational superannuation schemes for their workers.

In 1992, in response to the complexities of those systems and growing concerns about an ageing population, the government introduced the Superannuation Guarantee.

Compulsory superannuation was brought into law by Paul Keating’s Labor Government in 1992.

The Guarantee is the key feature of Australia’s modern super system. It is the piece of law that makes it mandatory for your employer to pay a percentage of your wage (currently 11.5%) into your super fund. When it was introduced, the World Bank described Australia as being at the “international forefront” of policies to address the costs of ageing.

How does superannuation work today?

Here are the key features of the system:

Employer contributions: Your employer must pay at least 11.5% of your ordinary time earnings (i.e., excluding overtime) into your super account.

Voluntary contributions: On top of this, you can put extra money into your super account, either individually or through your employer.

Growing your money: The money in your super account is managed by a Super Fund, which invests it in stocks, property, and bonds. Some people set up and manage their own super fund so they can have more say in how their money is invested.

Accessing your money: If you were born after 1 July 1964, you can access your super account once you turn 60 and have retired (or if you’ve not retired, once you turn 65).

Taking your money out: Once you qualify, you can withdraw it as a lump sum, an income stream, or a combination of both.

So these are some of the main features of Australia’s super system. Importantly, another component of this system is the tax breaks. These include:

You can choose to put up to $30,000 extra per year into your super fund, and these contributions are taxed at 15% when they go in. So if you usually pay 30% income tax, you’re saving (15% x $30,000 =) $4500 in tax per year.

The money in your super grows as you earn interest, dividends, or make capital gains through the investments made on your behalf. Recall what we said last week about the share market:

“If you buy a share in a company and that company does well, then your little slice becomes more valuable. You can sell it later for a higher price (that’s a capital gain), or sometimes the company gives you a share of its profits directly (that’s a dividend).”

These earnings are taxed, generally speaking, between 10-15%. Usually, these are taxed at your income tax rate.

If, when you retire, you choose to withdraw your money as an income stream and leave some money in your super, all additional investment earnings are tax free.

Ok, so the superannuation guarantee is increasing?

Yes, as of 1 July 2025, your employer will be required to put in 12% of your salary, up from 11.5%. Why? A few reasons, but a key one is that as we live longer, we are going to need more savings to fund our retirement.

And we are going to tax super balances over $3 million?

Maybe. The government has announced a policy to tax super balances over $3 million. It’s a complicated topic both in terms of how it would work and whether it’s a good idea. It’s too complicated to address it all now, but if you want me to unpack it let me know in the poll. In the meantime, here’s an explainer that Harry from our team wrote on the proposal.

A titbit for your group chat

In case you missed it, Taylor Swift has been dethroned as the world’s youngest richest self-made billionaire. That title has now been bestowed upon Lucy Guo, the 30-year-old tech founder of Scale AI.

Guo co-founded the AI business in 2016. It was most recently valued at $US25 billion, meaning Guo is now worth an estimated $US1.3 billion. On this, she told The Telegraph: “I think that maybe reality hasn’t hit yet, right? Because most of my money is still on paper.”

A message from EatClub

Superannuation might feel like a mystery for your future self - so here’s a saving you can enjoy today

While you’re figuring out how to grow your super, let EatClub help you keep your budget in check now.

Get up to 50% off food and drink at thousands of restaurants and bars around Australia. Just use the app, pay with your EatClub card, and watch the savings roll in.

It’s free, easy, and unlike your super account, you don’t have to wait decades to see the benefits.